Theatre Tax Relief Cashflow Loans

We offer loans to support non-profit theatres waiting for Theatre Tax Relief claims to be paid – so you can focus on strategic objectives rather than short-term cash management.

We offer loans to support non-profit theatres waiting for Theatre Tax Relief claims to be paid – so you can focus on strategic objectives rather than short-term cash management.

Image credits:

Photo by Liam McGarry via Unsplash.

Repayable finance is sometimes characterised as a tool for organisations in distress, but the dominant story across our portfolio is one of growth and strategic ambition rather than survival.

In April 2025, we published a blog setting out the four main ways arts organisations use the impact investment we provide – cashflow management, expansion of existing income streams, development of new income streams, and development of new funding models – illustrated with case studies. In this piece, we zoom out from those individual investee stories to a portfolio-level view across our three funds.*

It is best read as a spiritual rather than literal successor to the blog from last year. There are many sensible ways to categorise the uses of investment, and different taxonomies suit different purposes; the categories below differ from those used in the earlier piece, and that is by design rather than oversight, since in this piece we want to draw attention to the ambition towards income growth and financial independence on show in many cultural organisations.

We have made 62 commitments across our three funds: the Arts Impact Fund (AIF, 2015–2026), the Cultural Impact Development Fund (CIDF, 2018–2026) and the Arts & Culture Impact Fund (ACIF, 2020–2034). Of those, 57 have been drawn down, representing £16.7m of capital deployed into socially driven arts, culture and heritage organisations across the UK. Including the five commitments that did not ultimately draw (or have not yet drawn), the total committed sits at £18.8m.

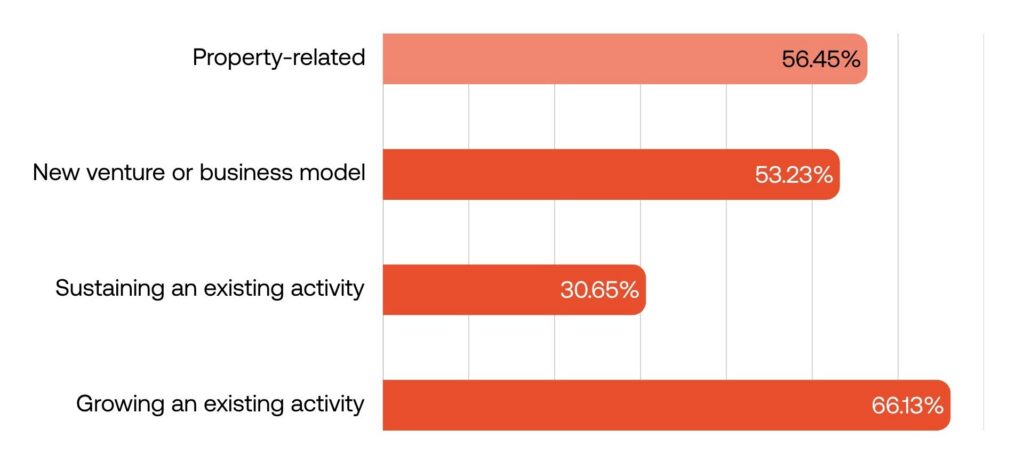

For this analysis, our investment team has coded each deal against four uses of investment, drawing on what borrowers told us they intended to do with the money. Three of the four uses describe what the investment enabled the organisation to do; the fourth is a different kind of category, describing what (some of) the money was spent on. We have grouped it alongside the other three because, as we will see, property and revenue-generating ambition tend to travel together:

The same investment can serve more than one purpose at once. That is true of most of our deals, which is why the percentages below add to more than 100%.

Three quarters of our commitments (46 of 62) involve at least two of these uses simultaneously, and 18 involve three or four. The most common combinations pair a property project with either the growth of an existing activity or the launch of a new one. This is intuitive once you spend any time looking at the deals: a building purchase enables sub-letting income; a refurbished hospitality offer becomes more efficient and more attractive; a fit-out creates rentable workspace that did not previously exist. Capital projects rarely sit on their own – they tend to be the foundation for new or expanded revenue.

The dominant story across the portfolio is one of growth rather than survival. Of our 62 commitments, 58 – or 94% – involve either growing an existing activity, developing a new one, or both. Only a small minority of our investments are primarily about getting through a difficult patch.

We think this matters for how the wider sector – and policymakers in particular – think about repayable finance for the cultural sector. Repayable finance is sometimes characterised as a tool for organisations in distress. Our portfolio data suggests that framing is wrong. Far more often, it is the route by which ambitious organisations make a strategic step-change: adding a revenue stream, acquiring or improving an asset, diversifying away from grant dependency, building the commercial muscle to support their artistic and social mission for the long term.

Used well, repayable finance is a policy tool for enabling enterprise in a sector that, given the right capital, has plenty of it.

These categories were coded by our investment team at the point of investment, based on what borrowers told us. They reflect intent and primary use case rather than an audited view of where every pound was eventually spent. The coding is binary (a deal either does or does not involve a given use) and so does not distinguish a marginal use from a dominant one. The headline patterns should be reasonably robust to those limitations, but precise percentages should be treated with appropriate caution.

For more on how arts organisations use impact investment in practice, see our April 2025 blog and the case studies in our portfolio. Find out more about the Arts & Culture Impact Fund, our open fund providing loans of £150k–£1m to socially driven arts, culture and heritage organisations across the UK.

*Figures correct as of June 2026.

Following earlier posts on financial resilience and how our investment has been used, we wanted to look squarely at what our money has pulled in alongside it.

On 2 July, around 20 practitioners working to fund culture and creativity around the world met to discuss the strengths and challenges of impact measurement and outcomes-based funding models.

In the second of our new Meet the Team series, we meet Theoni Androulidaki, Figurative's Investment Analyst, to learn about her background and work.

Seva Phillips introduces a new series encouraging candid conversations between practitioners financing culture in different parts of the world.